I feel a bit optimistic about the markets this week, at least in Ethereum land. Two days ago we broke out of a two week downward range, and this morning we broke one going back to mid-may, starting with the peak at $4300. And we’re above the 200-day moving average. We’ve got several resistance levels up from here, I’m looking for a close above $2900 before I feel really confident. Right now my Perp.Fi position is sitting around 4x with a liquidation price at $1580. I’ll probably maintain it here, using the negative funding to compound my position weekly, perhaps lower my leverage factor a bit. I think it’s safe to keep it here until new ATHs; I’ve still got enough cash in my bags to defend this position if we have another drawdown. I had enough stress dealing with liquidation risk last week. I’ll sit here.

ETHUSD chart

I still think we could range from here for the next month or so. We’ll see if EIP-1556 gets deployed on time, and what happens with the BTC price. Bitcoin has been somewhat anemic here, but on-chain data is really strong and there’s a lot of accumulation going on here. I’ve got two positions open here, 2x longs with liquidation prices at $22k and 18k. I’ll manage these for cash flow while compounding and looking for opportunities on LedgerX’s options or futures markets.

I’m not doing anything else in the market right now. I’ve been thinking about taking a position in PERP, but my main focus is income generation rather than speculation. I just moved $6,000 in USDC to my checking account, which will take care of my expenses through July at least. The historical funding rates on Perp.Fi are only at 75% my previous salary at my current nominal position value, so I’m either going to need the market to pick up 25%, or I’ll need to increase my size. I’ve got a couple ways I can do that. I can liquidate spot positions, harvesting tax losses while I’m at it, and convert that to Perp margin, increasing our decreasing the amount of leverage that I have in my position. A safer, but slower way to build this position is to remove the funding payments, which decrease my leverage and liquidation price, out of my margin, and use them to add additional leverage into my position, maintaining it over time.

I estimate that I have until the end of September to make this work. That’s when student loan payments come due, and I’ll need to make a decision on whether to take a regular job. In the meantime, I’ve got several projects I’m working on, hopefully one of them will work out and allow me to maintain my reFIREment indefinitely.

I had a couple calls earlier this week from a couple friends who want to increase their bitcoin holdings. One is an individual investor, and the second wanted to know how to best purchase as a group. I know this is only anecdote, but I think it goes to show that this latest pullback is being seen as a buying opportunity by many. This discussion will focus on Bitcoin and Ethereum-related assets. I’ll cover the individual case first and build out from there.

Dollar cost averaging

My first friend, R, is a successful professional who has less than one percent of their net worth in bitcoin, which they currently have in a Coinbase account. They want to increase their exposure with a five-figure purchase. Timing is important for R, they know we’re still early from a long-term, but worries that short term price fluctuations might give them a bit of stress. What I am recommending to R is that they open a BlockFi account and implement a dollar cost averaging setup to scale into a position over the next six months.

The benefit to using BlockFi is two-fold. First, USD funds on the platform are currently earning 8% APR, and the interest can be paid in BTC or other cryptocurrencies. Secondly, BlockFi allows recurring trades, which means R can set it and forget it while their fiat is converted to crypto. Six months from now, they can either re-up their cash allocation, or move funds to take advantage of more decentralized, on-chain solutions.

Exchanges

BlockFi, for all its benefits, has a couple drawbacks which make it ill-suited as a primary exchange for power users. It’s not really built for traders, and is only really good for the occasional swap. Also they discourage withdrawals from the platform with only one free withdrawal per month. Additional ones can run as much as thirty dollars. Plus they can take at least one business day to process, so woe to you if you need to move funds on a weekend. So you’ll need to open an account with a full-fledged exchange.

My wife recently asked me which exchanges I use to convert cash to crypto and my response was all of them. Literally. It’s hard to make a recommendation here as a lot depends on individual circumstances, like which tokens you want to trade, how you’re moving funds (wire vs. ACH), and your familiarity with trading interfaces. On the simpler end I’d put Coinbase, Voyager, and Gemini, with Coinbase Pro, Gemini Pro, FTX and Kraken on the other. Realistically, you’ll probably want to open accounts on at least two exchanges, one as a backup.

As a security precaution, you’ll want to make sure you set up two factor authentication on your account. Do not use SMS messaging as your phone’s SIM can be spoofed, use an app like Authy or Google Authenticator instead. And as an extra layer of security, you may also want to set up new email addresses for each exchange account as well. Using different email accounts other than your primary one will protect you should it get compromised.

Self-custody and hardware wallets

While centralized exchanges are the primary fiat on-ramps to the crypto ecosystem, there are custodial risks associated with them, hacks and outages being the primary ones. Most crypto-diehards will no doubt be screaming not your keys, not your coins at me or anyone else who suggests keeping large portions of your funds on BlockFi or any centralized exchange. Self custody is the way, and while there are a number of softwallets available for phones and computers, a hardware wallet is the way to go for significant sums of coin. I recommend a Trezor for most people, but anyone who plans on participating in DeFi, daos, NFTs or whatever else on the Ethereum ecosystem might want to take a look at the Lattice1, which has a large touchscreen for inspecting smart contract calls, as well as a host of other useful features. I don’t recommend Ledger products unless you plan on dealing with Solana, as it’s the only choice currently.

Lattice1 Hardware Wallet

An important note about purchasing hardware wallets: they should only be purchased from the vendor, and never from secondary markets. It’s recommended that you use an alias and a drop box for shipping to prevent your personal details from being exposed. Make sure the anti-tampering seals are intact on all the packaging. And make sure you generate your own private keys, never use any that have been given to you by someone else, and never record them in an electronic form. The Trezor will come with several slips for you to record your seed phrase, and the Lattice1 allows you to store your keys on a password protected smart cards. Either way, make several copies and store them securely in different locations to protect from loss.

Remember, if your device is destroyed or lost and you don’t have your private keys, or if anyone else gains access to them, your funds are lost forever. There’s no password reset button or customer service team you can contact if you forget this very important point.

Institutional accounts

If you’re buying crypto for a business, you’ll want to open an institutional account with an exchange. This could be for your LLC or partnership; I have a couple tied to my checkbook IRA account. You’ll need articles of incorporation as well as certificates of good standing from whatever jurisdiction that you’re registered in. You’ll also need to complete KYC for any authorized members of the entity that will have access to the account.

Now you’ve really got two ways you can go here if you are a corporation or business that wants to get into crypto. A lot of the big hedge funds rely on custodial accounts for their holdings, as dealing with self-custody is too much of a hassle for them. One of the most popular custodial firms is Coinbase, but I don’t have experience here to tell you much more. I can tell you that many of the crypto IRA products out there are basically built on top of Coinbase Custody, which charges an annual custodial fee as well as what I consider relatively high trading fees. You’ll also be limited to the assets that Coinbase has available. There are other custodial firms available, but again, I have no experience to speak of here.

Multisigs

This section is geared toward groups of people, whether they’re part of a formal corporate entity, or even an informal one. I’ll describe a couple ways that assets can be managed in a trustless way, that is, how a group can share management of assets, without allowing any one individual to have complete control of them.

The first, and most common is called a multi-signature wallet, or multisig for short. It’s a wallet in which a certain number of owners are required to sign off on a transaction before it can be approved, commonly referred to as m of n schemes, where n is the number of private keys associated with the address, and m is the number required for a valid transaction. These are most commonly configured as 2 of 3 or 3 of 5 setups, although you can have 2 of 2 or even 8 of 8 if you wanted to. There are a number of firms that provide bitcoin-specific multisig services, and it can also be configured via a Trezor hardware wallet and the Electrum desktop application.

There are no hardware based multisig solutions for Ethereum, although on-chain smart contract solutions do exist. The most popular is Gnosis Safe. With Gnosis, an on chain vault is created, and the m of n scheme and owners are specified. ERC20 tokens and NFTs can be sent to the vault address, and Gnosis has several plugins that allows the vault to interact with a variety of apps, such as Uniswap or OpenSea. Any owner can propose a transaction, and once the requisite number of owners have approved it it can be transacted on the Ethereum network. Many of the top defi projects on Ethereum use Gnosis vaults to manage their treasuries, and it’s a relatively trivial operation for less technical owners to approve transactions.

Other on-chain solutions

Gnosis is probably the most robust solution for a formal or informal group that is comfortable with a centralized, custodial solution. There are two others I’ll mention that might be more suited for other applications or groups, one that is non-custodial, and another that is decentralized.

The first is called Set Protocol. A Set is akin to a mutual fund, and can be created with anywhere between one and twenty assets within it. Users can issue Set tokens by providing assets to the Set, meaning that the value of each token is backed by the assets within the Set itself. They can’t be created out of thin air. The Set manager can perform a number of operations with these set assets, such as trading them for other tokens or providing them to a number of DeFi protocols. These actions are somewhat limited compared to what you can do with a Gnosis vault. While the manager does not have direct access to the funds in the Set, there are a couple ways that a manager can potentially exploit funds in the set, whether through changing the management fee or trading into a illiquid shitcoin, the manager address can be assigned to a Gnosis multisig for additional security. We used Set Protocol for the Homebrew.Finance $MUG NTF Fund.

The last one I’ll mention is DaoHaus, which is used to manage decentralized autonomous organizations, or daos. Daos are basically on-chain shareholder corporations, and are useful if you want to create a trustless organization. Users can deposit into the dao in exchange for voting shares or loot, both of which grant proportional ownership of funds in the dao’s bank. Many of the popular daos on DaoHaus are venture funds or non-profit/open source grant foundations. Users can create funding proposals, the membership votes, and funds are distributed accordingly. Managing a DaoHaus can get a bit complicated, but it can also be combined with a Gnosis safe to provide more accountability. Additional development on DaoHaus minions, or associated smart contracts, continues to add more functionality to the system. We are using DaoHaus to manage membership in SAIADao.

Wrapping up

One quick note about on-chain Ethereum solutions such as Gnosis and so forth: gas fees. Congestion on the Ethereum network lead to some pretty high transaction fees over the last few months. It cost me over $500 to create the $MUG Set, back in March, with trades costing over $150 each. Creating a Gnosis safe cost me over a hundred dollars earlier this year after gas had come down, but the vault overhead does add some overhead to transactions. I wouldn’t recommend them unless you’re dealing with several thousand dollars worth of funds. Thankfully, the release of other Ethereum-compatible sidechains such as Polygon and xDAI are making relieving some of this pressure, although a full discussion of this will need to wait for another day.

Hopefully this article is helpful for others who are looking to increase their exposure to Bitcoin or Ethereum-related assets.

Well the past twenty four hours have been a roller coaster. I got way to cocky with my leveraged ETH long, and I’ve been on the verge of liquidation twice today, both times I added more collateral to the fire in order to stave off disaster.

I’ve been playing the funding game on Perp.Fi for the last week or two, setting up some conservative long positions to make some income on the negative funding rates that are available. I’d been doing pretty good for a while with my 1.5x BTC position, then I went and got all stupid with a 4x ETH long. I apparently forgot what happened to me last time I pulled some shit like that. So last night I went to bed, disgusted at myself and telling myself that I deserved to get liquidated for the $8k that I had laid down as margin. I had a little trouble falling asleep, but slept well and woke up with it on my mind. I didn’t want to know.

I told myself I was cool with the loss, and held off looking at the chart while I did my morning routine, but I accidently saw the chart when I unlocked my phone. I was right at liquidation. I meditated on the best course of action to do, veering between doing nothing and adding more fuel to the fire. I tried to figure out what the best course of action was. I went for a two and a half mile jog to clear my head, then finally went upstairs, pulled a few thousand out of my BTC position margin and threw some of it at the ETH position, trying to bring them somewhat into parity. I think I was actually in a liquidatable state when I did it. I guess the bots had bigger fish to fry. Lucky me.

So I spent a lot of time staring at the five minute chart again today. I managed to get several hours of work done on some Rust challenges, but I kept looking at the chart every couple minutes. As the day went on and I got interrupted more and more with the kids it became harder and harder to concentrate, but I managed to get a lot done. Plus I did a lot of cleaning and cooking. But the precariousness of my position plus some trouble with the girls put me a bit on edge, so I lost my temper a few times. Missus saw my stress and asked what was wrong, so I told her, then went and cut the grass.

I came back in and commiserated over the situation, watching the chart. In a way it would have been better if I’d been washed out in a quick scam wick. Just put me out of my misery. This long drawdown is going to suck in more and more of my capital to keep the position alive. I don’t know how far down I can go, but sunk cost fallacy is surely a factor right now. It’s my fault for not having a plan for this. Surely ETH can’t go down $2000 again! The whole situation makes me fear about how low BTC can go. If this crap goes on too long I’m going to wind up liquidating everything in my portfolio just to keep this long going.

A few minutes ago the price got really close to my liquidation price, so I put another $1000 in margin, giving me another couple hundred dollars reprieve on my liquidation price. I’ll sleep better, and who knows, maybe I’ll see a reprieve and make it out of this alive. What a mess. This is definitely not how disciplined trading is supposed to work.

So I’ve been experimenting with Perpetual Finance for about a month now, and after today’s BTC pump over 40k I finally decided to take the plunge and invest a significant amount on the platform. Also, I won their Pool Together lotto.

PerpFi is an on-chain, decentralized perpetual contract for crypto assets such as bitcoin, ethereum, and DeFi blue chips. They offer up to 10x leverage, short or long, and use the xDAI network for super low transaction fees. All trades are denominated in USDC, and they’re offering no-gas bridging if you move more than $500 over to the xDAI network. They have a governance token, PERP, and also provide trading rewards in the form of a Pool Together token which pays out in PERP tokens. This is how I won the lotto.

Perpetual contract are a type of financial instrument that is native to crypto. It’s similar to a futures contract, but the difference here is that unlike traditional futures, perpetuals do not have expiration dates, meaning that one can long or short an asset and hold the position indefinitely. FTX and dydx are two centralized platforms that provide perpetuals, Perp.Fi is the first decentralized on-chain platform for this.

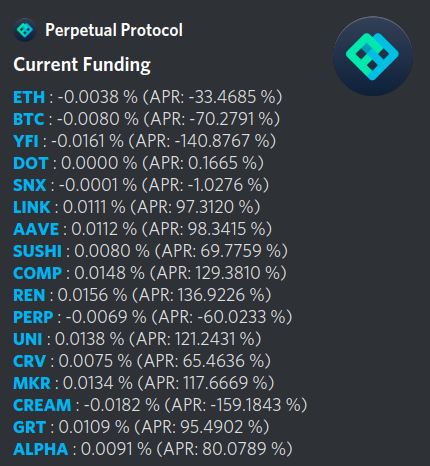

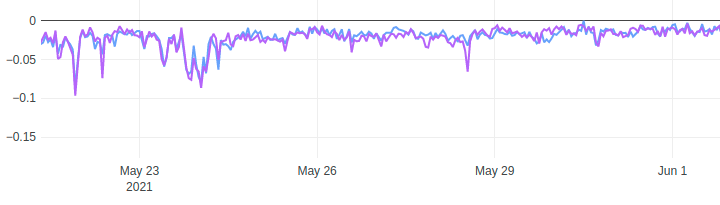

Since perpetuals allow leverage, there are funding costs associated with positions. These costs are determined by the difference between the price of the perpetual contract and the oracle spot price. If the perp price is below spot, then a premium is paid to those who take long positions. This is how our strategy works. Here’s a snapshot for all the current Perp.Fi trading pairs:

Again, anything with a negative rate is actually generated by shorts paying longs. Rates were actually a bit higher today, around 133% for ETH. For ETH and BTC, historical rates have always been negative, due to the fact that Perp.Fi is primarily used to short these assets.

ETH and BTC funding rates on Perp.Fi

I first started experimenting with Perp.Fi about a month ago, taking out a few 5x long positions on ETH and BTC. 5x is actually kind of aggressive for a long-term position, and I actually wound up getting partially liquidated a few weeks ago when we had that dip late last month, losing about a third of my position. Since then, however, the funding rate has almost paid back what I lost. And since one can take an un-liquidatable 1x long position on Perp, it’s pretty much a no-brainer for me to move my wBTC positions out of underperforming yield farms and put them into Perp. I’d also argue that Perp.Fi makes more sense than holding Index Coop’s ETH and wBTC 2x FLI tokens, since they both suffer from a 2% management fee as well as funding expenses from their underlying components.

Recently I’ve been experiencing a bit of anxiety over a bit of underperformance in my stablecoin reFIREment fund. I’m short on cash and was facing the prospect of having to spend some of my stablecoin yield farms. I think these perp contracts may have given me a way to not only stave off dipping into those funds. I’ve opened a low-leverage, 1.5x position on the platform, equivalent to my annual expenses. The funding, it if maintains a 100% APR, will allow me to remove margin from my account and send it to my expense account. Perhaps a bit more explaining is necessary.

Let’s say you do as I did today and open a 1.0 BTC position with 1.5x leverage at $40,000. Your upfront capital is $40k, but you’re actually holding a $60,000 BTC position. The funding rate is based on your position size, not your margin, but the funding is paid to your margin. So while you might initially start your position with a liquidation price around $15,000, as each hour passes, the funding rate will lower your liquidation price. Perp.Fi allows you to add or remove margin, so you can actually remove margin over time, keeping your liquidation price steady, and allowing your to either add to you position or cash out. Herein lays my strategy.

I’m hoping that the funding rate will be sufficient for me to maintain this low-leverage position indefinitely, removing the funding proceeds from my margin. Of course the rate is variable, so I’ll be keeping a close eye on things. And of course there’s the risk from carrying a leveraged position, both from price volatility and liquidation risk. That said, I think the bottom is in an there is zero chance that bitcoin goes below 20k. (Famous last words.) If I wanted to be more aggressive I could remove more margin and lever up my position, but I think I have a somewhat conservative position here that is mostly risk free and will allow me to pay my mortgage and grocery bills.

This is either a galaxy brain move or is going to get me rekt:

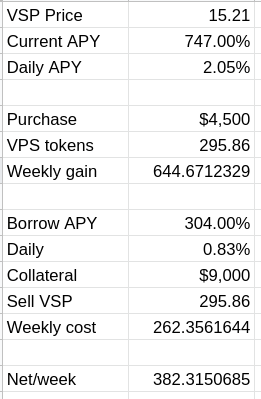

I’m trying to find a way to generate some income for myself. Since it looks like the market could go either way right now, I’ve been looking for a way to generate yield in a market neutral way. Traditionally, one would do this by buying one asset and shorting it at the same time while capturing the spread. Vesper’s vVSP pool has a quite insane APY, so I wanted to see if I could capture enough off of this to cover living expenses, and decided last night to try a position for a week. So I staked my Yearn Iron Bank position as collateral on CREAM and borrowed VSP, which I then staked on Vesper. The borrow APY is quite ridiculous as well, but if my math is right, I should net a couple hundred dollars this week.

It’s not quite enough to live off of, but it should open doors for other similar strategies if it pays off. Since my collateral is in stablecoins, my main risk is that the price of my borrowed asset appreciates and puts my collateralization ratio at risk. Due to the current VSP issuance rate, I don’t believe it’s at risk for some sort of pump. Regardless I think reduce my risk by restaking the VSP back into CREAM, but I’m really not sure about the secondary effects of that. It might put me in a position where I’m stuck and might need additional collateral to rotate out.

My plan is to let this ride for a week, remove some of the staked vVSP, swap some of the VSP to USDC and use the rest to pay back the interest on the debt. Gas costs will be a factor, as will changes to the VSP APY and CREAM lending rates. If it works, I’ll be able to generate cash flow and not be concerned if the price of VSP continues to drop.

When VSP’s emissions rate dies down enough that it’s no longer providing me with enough incentive, I can try other pools. CREAM has a huge number of assets available to borrow, I just need to figure out the best opportunities for them and figure out where to go. UNI is only 3.55% to borrow right now, and I could stake that on Impermax for 57% currently. That’s probably more risk than I’m willing to take on, given that protocol’s only a few weeks old.

I’ll have to look at some other platforms as well to try and figure out other ways I can generate some yield while staying market neutral. Since I’m mostly in stables, ETH and wBTC, I’m sort of in a bind, since returns on ETH/wBTC are pretty lousy across the board, and borrow rates on stables are already pretty high. All told, I’m not sure that this is a viable long-term strategy, but I’ll continue to investigate. I just don’t think I’ve got enough capital to make it work unless I am willing to put a lot of my eggs in one basket. It may be to risky a strategy to pursue.

I was pretty busy yesterday, as I got the latest tranche of funds transferred from my brokerage TradFi IRA over to my AltoIRA and onto Kraken. Tracking my portfolio to my original plan was very difficult, due to the various wallets, chains and apps that I’m using to track it. My original plan was to do a 40/40/20 BED portfolio, (BTC, ETH, DPI,) but it’s changed a bit. The current portfolio looks a bit like this:

BTC

16.75%

Native BTC

wBTC

18.25%

also includes BTC2x-FLI-wBTC SLP

ETH

31.00%

also includes ETH2x-FLI

DPI/BDI

7.50%

Staked BDI, BASK

ALCX

6.50%

Staked alUSD, ALCX and ALCX-ETH SLP

Solana

8.50%

SOL, SOL-RAY and STEP-USDC LP

USD stables

5.00%

Other

6.50%

BAL, RUNE, others, Star Atlas NFTs

I can’t actually seem to get the total value of the other category to calculate correctly, leading to a margin of error around five thousand dollars. It made trading a little bit difficult, since I wasn’t quite sure how to balance what I was doing. So I’m sitting on about seven percent more cash than I want to right now, and was not sure exactly how to proceed, so I made a few trades into ETH and wBTC, sent some USDC to Solana, and decided to look at some other things.

I’m not quite sure what brought me to it, but the V1 Yearn 3crv vault is migrating to the V2 version and is not earning boost, so it needed to be moved. I decided to pull it entirely and move it to the native USDC vault, which is getting a higher yield right now. I came out a bit ahead, thankfully, but only a trivial amount. I’ll have a full report on the reFIREment fund in June.

I did start poking around the other Yearn vaults while I was there, and contemplated the yvBOOST vaults. It basically holds yveCRV tokens, which go into a one-way vault, and earn 3crv tokens in return. The BOOST vault compounds these of course, but there’s another one that interested me was the one that deposited it as yvBOOST-ETH SLP on Pickle.Finance. The first time I looked at it a few weeks ago I couldn’t wrap my head around it, but this time it clicked. I’ll explain, with a slightly different example. I’m holding ALCX-ETH SLP, which I have staked on Alchemix for more ALCX rewards. I unstaked my SLP from there and deposited it on Pickle, where the jar, or vault, follows a basic auto-compounding strategy. This turns my 250% APY into a 500% position. On top of that, I can stake this resulting pSLP, as it’s called, for an additional 10% APY in PICKLE tokens.

I also spent a lot of time on Perp.fi yesterday. I’ve been trying to wrap my head around perpetual contracts for some time, but have been somewhat limited as a US-citizen. I’ve done some basic leverage trading on Kraken, but found the experience to be a bit lacking. FTX.us has some leveraged products available, but using margin with my IRA triggers a taxable event, and I haven’t done KYC with my regular account yet. Perpetual Finance, while still geo-locked for those of us in the US, is available 100% on-chain. Better yet, it’s trade engine is on xDAI, which means it’s very cheap to use.

Even better, funding rates are negative, meaning that shorts pay long. So I can basically get paid to take a long position. Everything’s done through USDC, and I already had some wETH and wBTC on xDAI, so I liquidated some of my position and opened longs using the proceeds as collateral. So I’m sitting on a couple of 5x positions, that won’t get liquidated unless we have a further market correction that takes us lower than this week’s lows. In the meantime, I’ll get a little bit of funding from the spread.

I’m really impressed with the Perpetual team. Their docs are put together nicely, and their code repos have some nice treats, including a CLI client (!) and an FTX/Perp arbitrage bot, which is nice. They have their own token, which receives some of the trading fees, but I haven’t decided whether to take a position on that. The main use case seems to be for taking short positions, as this video shows. Taking a market-neutral position to facilitate high interest yield farming really opens some doors.

Perp is limited to a few trading pairs, mostly BTC, ETH and a few DeFi blue chips. One really important note in the video is how you can use CREAM’s bigger selection of tokens to short the other side. I clicked with me, and opened up the door to another piece of the yield farming puzzle. I’ve got plenty of tokens and LP I can use as collateral in CREAM and borrow some of the low interest rate tokens, such as DPI, and, which I can lend to Impermax; or VSP, which is 25% to borrow, but yields 125% in the Vesper vault. There’s obviously some liquidation risk, but it is something I’m going to be taking a further look at in the coming days.

The crypto bloodbath continues today, with ETH breaching $3000 and BTC $40k. Suddenly my 2x FLI positions aren’t looking to shabby. The market is a complete mess, everything is a sea of red. Still, I have a transfer from my brokerage IRA that is almost complete and should be on exchanges either today or tomorrow, so I will be ready to do somme discount shopping. Still, I could not have picked a worse time to retire. My goodness.

I’ve started working on Solana in earnest, working my way through the tutorials for Anchor, their deployment framework. I have got to get multisig working, as SAIADao has raised over $58,000, and I’ve got close to nine grand in a soft wallet that only I control. Setting it up seems a pretty straightforward procedure, it’s just a program, but it’s using it that I’ve yet to figure out. I have no idea how to interact with Serum via command line, so that’s going to be something new for me to figure out.

Since SAIADao has done so well, I’m moving the timetable up to start purchasing posters in about two weeks. We’ve got more than enough to cover the Star Atlas: Rebirth Tier 3 posters six through eight and have plenty left over. Still, I’ve been making mistakes with some of the proposals, sponsoring some before I verify the wallet transactions, and I even let one through today for five grand that had the parameters mixed up. Thankfully someone caught it, but now we’ve got to vote it down so that it can be redone. It’s a bit of a mess, but I should be able to step back a bit and let others do it.

I’m having trouble bringing myself to work on … work. I had a meeting yesterday with the St. Louis crew that I forgot between my morning call and 1PM. By that time I was doing school work with Younger and didn’t check my work computer until almost three. There’s a lot of other things that I seemed to be missing as well. I just got seven more days to go, but I have absolutely no motivation to do anything at all. There’s too much else going on in my life that has a higher priority. For example, I haven’t been able to get in touch with my dad for several days, last I talked to him was the day after his second surgery. Just put that on the to-do list, I guess.

Someone turned me on to this new game called Core. It’s a very cool concept, it’s like Roblox in that you can build your own games with it, but it’s built on the Epic Games platform, so I assume it uses Unreal engine. It’s got an editor that’s very similar to Unity and Roblox, but the main difference is the number of game assets that are made available by default. There are even frameworks for dungeon crawlers and capture-the-flag games, I was very impressed with it. There’s also a central hub that players can hang out in, and jump into portals which take them to the games. They load very fast, and the entire process of jumping from game to game is very seamless.

Of course I wanted Elder to check it out with me. She’s of course more interested in playing the games than building them. Core is geared at an older teen or adult audience, so I don’t know if I’m pushing her too hard, but I’m hoping we can find something to work on together, but I’m not sure if it’s going to take. I’m going to start her with Galileo in a couple weeks, so we’ll see what she takes after then.

I’m hoping that I’ll be able to spend a lot of time with the kids over the summer. Working from home while trying to be Mr. Mom has been really stressful for all of us, mainly as they have no boundaries when it comes to interrupting me when I’m on the phone. I’m sure there’s something to be said about my lack of balance in the past, but that’s all about to change dramatically in a few more days.

CPI inflation beat all estimates; Vitalik rugs SHIB and other meme coins; Elon dumps Bitcoin over “dirty power”, bitcoiners fight back.

I don’t have much insight on these inflation figures but am just throwing them here for informational purposes. We’ve known asset inflation was already here, as I discussed yesterday, but I did not see this change in the CPI coming so fast, nor did I expect it to hit four percent already. Most of the macro people I follow have been anticipating this for some time, the question is where do we go from here. Bullish BTC.

Inflation numbers blowing past expectations, leaving every single economist estimate in the dust

4.2% year-over-year change in the CPI vs. 3.6% median estimate.

So Vitalik Buterin, the founder of Ethereum, gets lots of airdrops. Apparently token creators do it as some sort of social proof, as they can later say that “Vitalik is an investor in our project”. This happens to Mark Cuban as well as any high profile whale address like the 0x_01b address or whatever it is. So that’s how Vitalik wound up owning about $8 billion dollars in SHIB. These dumbasses decided to drop him Uniswap LP tokens instead of just locking them up in a timelock like most people. Vitalik’s been in a very tough conundrum, a trolley problem, as one person described it. Holding the token was bullish for SHIB, and could lead to more nonsense. Selling it would hurt a lot of people. Damned no matter what he did.

The final straw was several days of network congestion on Ethereum, as gas prices remained in the 300-400 for several days. Most of the traffic was SHIIB, as well as several other clones that sprung up. Even Binance chain was affected and required people to increase gas. So VB did what he had to do, and dumped it. All of them.

— Igor Igamberdiev (@FrankResearcher) May 12, 2021

You should really look at the thread above . He removed the LP, then started dumping and donating coins to charity. SHIB, AKITA, and ELON were all either dumped or given to charities including Gitcoin and a COVID relief fund for India. One person pointed out that he sent the meme coins to the charities, while keeping the ETH for himself. What this means is that he was able to deduct the full value of the meme tokens as a charitable contribution, even though the charities would in no way be able to redeem the tokens for that value. There’s just not enough liquidity or depth to the market.

This seemed to trigger a minor pullback in the price of ETH, but that was nothing compared to what was about to happen. Queue memelord Elon Musk:

This caused a huge dump in the BTC price from $54-46k in a matter of hours as billions of leveraged traders were liquidated. Much of it was quickly bought up, and it’s recovered to the 49.6k level as I write this. Many were quick to point out that anyone with enough BTC to actually buy a Tesla were unlikely to spend it on one, so Elon wasn’t shooting himself in the foot here. There was also speculation that Elon may have been pressured by bitcoin critics on the environmental front, and that he doesn’t really believe the Tesla statement personally. This article provides some additional context.

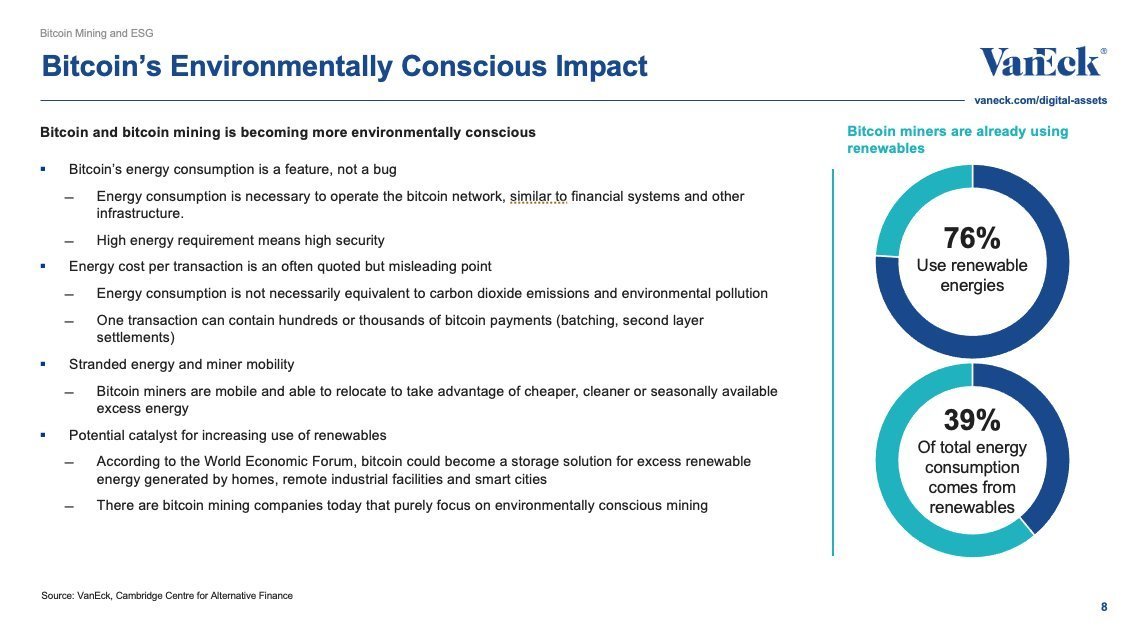

The Bitcoin community is taking this accusation as a call to arms. For months, there has been misinformation about bitcoin’s environmental impact being circulated, and this Tesla tweet is the last straw for many. Many believe that bitcoin production actually creates more demand for renewable production as well as the capture of waste energy. Many bitcoin farms rely on hydroelectric, and there are companies that are capturing waste methane from gas mining rigs, which would normally be vented out into the atmosphere, to power bitcoin mining equipment. Bitcoin mining can also smooth out troughs in power demand, coming online when demand is low and shutting down when it goes back up.

Of course that’s not to say that some bitcoin production relies on fossil fuel. The Tesla statement is apparently referencing a Chinese coal plant shutdown last month that was accompanied by a significant drop in the bitcoin hashrate, which was apparently due to the fact that hydroelectric power supplies had caused many Chinese miners to shutdown and relocate following the rainy season.

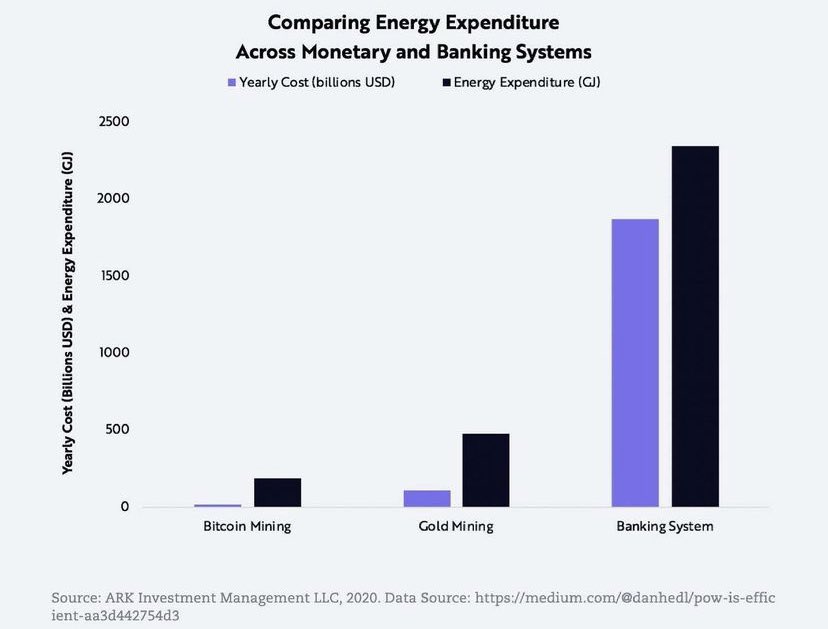

Bitcoin is an easy target for many due to the fact that the hashrate is available directly on chain. While critics like to bemoan the fact that the bitcoin network uses more power than most small countries, it’s not a fair comparison. No one talks about the current environmental impact of gold mining production, or the combined cost of paper currency production by every nation on earth. Those figures aren’t as easy to come by. Thankfully, Ark Invest has done the math for us.

Of course for many bitcoiners, the cost of the fiat monetary system is way worse than the environmental impact of bitcoin. If we are returning to four percent inflation, or higher, then people are going to witness firsthand the damaging effects of wealth destruction, as peoples’ savings are destroyed by rising prices. The next few days will likely see bitcoin’s energy usage at the front of debate, and hopefully this time it can be put to rest.

Thoughts on Weimar, meme coins and the end of bullshit jobs

So ETH broke $4200 as the world has lost its mind over meme coins. SHIB is some multi-billion dollar token now, and new competitors are springing up left and right. Gas on ETH is the lowest I’ve seen in days, 180 gwei as I write this, but I still have yet to make any moves on mainnet in roughly a week. It’s just too expensive. My OpenSea listings remain untouched, and likely won’t fill since it’s just too damn expensive to do anything.

I think we go up from here. Sell pressure on ETH is likely to be non-existent for some time, given all of the staking options that are happening. Bankless has gone into this whole ultra-sound money thesis a bunch so I’ll not repeat it here, but Cochran’s tweet below is likely correct. NGU technology indeed. And I love that he lumps his investments into EVM-compatible and Solana. Confirmation bias indeed.

1/11

A lot of people are expecting the next 'segement' of this cycle will be outflow of ETH profits (which added $200B to its mcap this cycle) into DeFi tokens (which all collectively are worth only $150B)

I think the DeFi tokens are the next play, but outflow isn't the signal

— Adam Cochran (adamscochran.eth) (@adamscochran) May 11, 2021

My thesis for this cycle has been that ETH would outperform BTC. When ETH hit $2000 I put a good amount of my retirement portfolio ETH into the ETH 2x FLI token, at $123. Today it’s at $420, and I’m sitting pretty. I’ll likely hold this position until ETH breaks this line, then I’ll consider scaling it back a bit.

Messari’s Ryan Selkis made a comment a while back that we’re likely to see a lot of “idiots” making more money than us this cycle, and he cautioned that it was OK and not to follow the FOMO. There’s plenty of money to be made this cycle, one just needs to keep their cool, follow their plan, and execute. There’s just so many people flowing into crypto this time round, there’s no telling how crazy things can get from here.

One thing that does have me concerned is the broader casino quality that’s going on now. I don’t know how much of the broader population is entering the space right now, but I think we might be in for trouble long term if we start minting millionaires left and right. I don’t know how many low-wage workers are winning the lotto with Doge and SHIB and all these other meme coins, but I hate to see the fallback once this bubble busts. I remember the feeling of anxiety and excitement that I felt during the 2017 run as I watched my four figures become size, but I also remember the anxiety and doubt that occured as the market corrected eighty percent over following six months.

There’s been a bit of fear-mongering among some conservative and libertarian media about people making more money on unemployment benefits and stimulus than they would make working at most jobs, and we know we’ve been facing a skilled labor shortage here in the US for some time. A good number of my clients over the years have been struggling to find skilled labor. HVAC techs are just one example I can think of. Now I’m seeing reports on social media of fast food restaurants closing down with signs taped to the intercoms that “no one wants to work here” or “people don’t show up for the jobs they signed up for”.

And I can attest that certain types of tech roles are hard to fill these days. Take mine for example. I’m basically forfeiting my position to work for daos or protocols or yield farming or whatever the hell I’m going to call it. Is this the future of work? Is the rise of SHIB and meme tokens going to spawn an exodus from productive labor? in the past I’ve pushed back against the idea that stimulus and UBI would lead to the mass exodus of labor from the market, at least a detrimental one. Sure a lot of bullshit jobs are going to be really hard to fill moving forward. No one wants to work for a minimum wage job when it takes three or four hours of labor to feed a family of four from the same restaurant.

After reading When Money Dies I’ve got a few doubts. So much of what that book describes in 1920’s Germany seemed oddly familiar to me when I was reading it, and each day that goes by seems to be like deja vu. The rush to speculative assets for example, the realization that it’s not the assets themselves that are going up in value, but that our money itself is losing value. In this case it’s not just the dollar, but all fiat currencies that are losing value against Bitcoin and other cryptoassets. We’ve already seen asset inflation in stocks and the housing market; used cars experienced a bubble last summer as stocks of new cars fell off due to factory closures; the price of lumber is still exorbitantly high due to home-improvement and new construction demand. Now, as the economy returns post-COVID, we’re seeing the beginnings of a bubble in energy stocks as demand meets a year of underproduction. Not to mention the shutdown of the Colonial Pipeline due to a ransomware attack that has led to gas station shortages.

We are in the beginning of the euphoria phase of this bull cycle, I would say. One recurring theme from When Money Dies stands out to me, it was that through the multi-year collapse of the mark in Weimar, things kept getting worse in an unending catastrophe, again and again and again. Crypto, with its charts and cycles, might be giving us a better view of exactly what’s going on. As the market cap of these coins go parabolic, we can always wonder when the pullback will begin, when the correction will come.

ETH broke $4000 early this morning, and with gas at 250-300 gwei, it has become painfully apparent how difficult it is going to be to continue to operate on Mainnet for the coming months. Yesterday a simple ERC20 transfer was about $180 in gas, and I’m pretty much putting a hold on all ETH activities unless I carefully consider exactly what I’m doing.

Everything under $400 in value is effectively dust for now. We may see some relief briefly once Optimism launches, but I think long term, if ETH is going to $5000-10,000, it’s going to price most participants out of the market. I’m almost there myself. I’m trying to triage my positions into several buckets.

Dust: shitcoins I bought as a crapshoot, that have no real value to justify swapping them back to ETH. I’m not sure what I can do to deal with the tax ramifications of this. I can’t merely mark them “abandoned” unless I burn them or the private keys for the wallet. The latter is unacceptable for a variety of reasons, I’m not sure what else can be done about this loss. It will need further research.

AMM only coins: Coins that are worth a couple hundred bucks, but don’t have any liquidity off-chain. I’ve got a couple things I can do here. One, if I believe in the project I can just hold on, which is the most risky option, or I can swap close the trade and take ETH/stablecoin profits. Alternatively, I could bridge them to a sidechain, Polygon, BSC, or Polygon. This might not be as expensive as an AMM trade, but it also depends on liquidity as well.

Majors: Most of the blue chips have plenty of options for trading, so it might make most sense to move these coins to Kraken or one of the other centralized exchanges. L2s are also an option, but migration is a bit more expensive than just an ERC20 transfer. It all depends on how comfortable I am with custodial risk. There are a couple ways to reduce cross-chain transfers fees. FTX has free transfers to Solana, and Binance can do the same for BEP20 tokens. It seems kind of ironic to set up to sell ETH on Solana, but no more so than doing wBTC on Ethereum.

Then there’s the whole what to do with my yield farms. Obviously, harvesting is going to slow down a lot, and there’s a lot of yields that aren’t going to be worth the gas to claim. I’m going to be thinking very hard about what I do in the coming months. And moving into new positions… well, that’s going to be a very hard decision to make.

I think there’s probably one project that I’m even remotely considering getting into. OlympusDAO seems almost too good to be true, like Alchemix, so I’m going to wait for an opportunity for gas to come down and then throw some funds into it.

Basically I’m looking for things that I’ll be comfortable staying in for the next three months. Or longer. I don’t know how the Ethereum community is going to deal with the prospect of five-figure ETH, and what that might mean for the network. If it’s going to continue to be the type of network that can run a node on a laptop, then they’re not going to be able to increase the blocksize too much bigger than they have now. Still, I’m not able to make a prediction as to what the long term effects on gas is going to be. Optimism and the upcoming EIP may reduce short-term gas issues, but if ETH continues to climb, then Ethereum will continue to price people out of the market, forcing participants onto side chains.

![What is a Decision Tree and How to Make One [Templates + Examples] - Venngage](https://venngage-wordpress.s3.amazonaws.com/uploads/2019/08/ad-mistake.jpg)